Some European countries and emerging markets are now showing signs of slow recovery, as the Covid-19 pandemic brought overseas markets to a shuddering halt in late March. However, demand is expected to remain weak through the beginning of the third quarter, writes PV InfoLink’s Amy Fang, as it will take time for overseas markets to snap back. Meanwhile, the Chinese market is again busy with the June 30 installation rush, as the government has left tariff timelines unchanged up to the middle of May.

From pv magazine 06/2020

Cell prices have bounced back, and module manufacturers raised utilization rates at the end of April. But this rebound will be short-lived because the majority of projects to be installed by June 30 are delayed from 2019. Prices across the supply chain are likely to trend downward.

Market movement

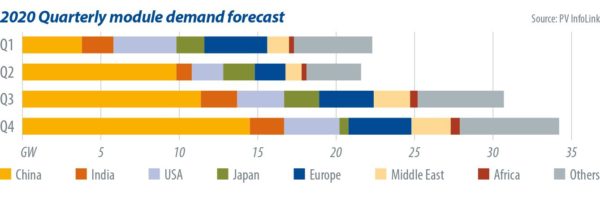

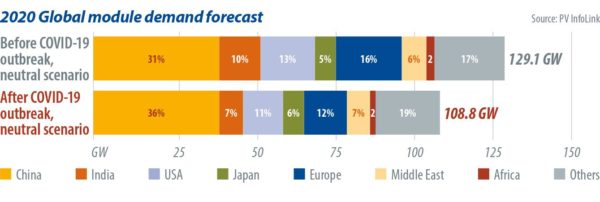

From a demand perspective, most overseas projects had secured financing prior to the virus outbreak. To ensure the smooth development of projects, countries around the world have either extended grid-connection deadlines or postponed auction schedules, although most struggled to provide an exact new timeline at the beginning of the outbreak. With the pandemic gradually easing in some European and Middle Eastern countries and lockdown measures slowly relaxed, some have confirmed new schedules. As countries are lifting lockdown measures cautiously and in phases, the progress of project installation is slow. PV InfoLink has revised the projected share of overseas markets from 69% to 64% this year.

While overseas markets are suffering negative impacts of Covid-19, demand in China is relatively stable. Because of a delay in openings, the Chinese market was anticipating an extension to commissioning deadlines. However, the government had not released any notice regarding the matter as of late May.

Against this backdrop, developers began rushing to install systems in May to secure payments by June 30. Meanwhile, installation of Top Runner Program and ultra-high voltage projects is continuing as the government shows no intention to change deadlines. While Chinese demand is projected at 10.7 GW in the second quarter, the June 30 installation boom contributes around 6-8 GW, meaning that the pickup in demand will be short-lived. PV InfoLink maintains its full-year demand forecast at 39.5 GW. With demand in overseas markets remaining weak in the second and third quarter, China’s role in sustaining demand grows more important.

On the supply side, disrupted logistics and bill of materials shortage caused by the pandemic started to be felt by module manufacturers in the middle of the first quarter. As workers returned, operations resumed, and transport hiccups were resolved, Tier-1 module manufacturers were operating at 60-80% utilization rates during the first three months of 2020.

Module deliveries, however, have been disrupted since April due to deferred demand in overseas markets. With India imposing national lockdown, the Middle East enforcing curfews, and Europe remaining closed, deliveries were unable to be made as scheduled. As a result, module manufacturers stopped outsourcing and lowered utilization rates. Tier-1 manufacturers were originally expected to cut capacity utilization by 10-20% during April and May, but the return of the June 30 installation rush helped companies that have higher share in the Chinese market to boost sales, with top 10 module manufacturers operating at higher-than-expected utilization rates.

Among those that planned to lower capacity utilization, many reduced at a smaller scale or even operated at full capacity. As overseas demand continues to stagnate, Tier-1 module makers will maintain a utilization rate of around 80%, whereas Tier-2 players will operate at 30-50% due to lower order volumes – a result of disadvantages in branding, channels, and costs when comparing with Tier-1 makers. This is evidenced by the dominance of Tier-1 module makers in the second quarter, in which overall module production volume did not change much from the first.

Consolidation creeps

Without branding or cost advantages, Tier-2 module makers struggled to compete with their Tier-1 rivals in the Chinese market. Having secured the majority of orders, the top 10 module giants have kept their shipment targets this year unchanged. It’s certain that the module segment will see even more consolidation under the impacts of Covid-19. Moreover, module manufacturers are ramping up capacity as wafer sizes are changing rapidly, with more than 56 GW of new capacity expected this year. Older capacities will be eliminated along with the capacity expansion. This has made it difficult for Tier-2 manufacturers to survive when demand remains persistently low. Manufacturers without competitive edge may turn to subcontract work or withdraw from the market. This year is expected to see significant growth in the market share of top 10 manufacturers.

The return of the installation rush to meet the June 30 deadline will help reboot the supply chain, but only for a short period of time. The results of project auctions in China announced in the middle of May suggest that a price war among Tier-1 manufacturers to secure orders has already begun, with bid prices falling to record lows. The downward trend in module prices will continue into the second half of the year. In addition to the aforementioned short-lived demand from the June 30 installation boom, oversupply and with it price declines resulted from the continuous ramp-up in module capacity and limited elimination of older capacity. It’s expected that prices for modules will decline from $0.2-0.203/W to $0.195-0.198/W over the second to the third and fourth quarter. The downward trend may not stop until the high season returns in the fourth

quarter.

Lắp đặt điện mặt trời Khải Minh Tech

https://ift.tt/2X7bF6x

0906633505

info.khaiminhtech@gmail.com

80/39 Trần Quang Diệu, Phường 14, Quận 3

Lắp đặt điện mặt trời Khải Minh Tech

https://ift.tt/2ZH4TRU

Không có nhận xét nào:

Đăng nhận xét